Disclaimer: This article is for informational purposes only and does not constitute financial, investment, compliance, or legal advice.

Why 2026 Is a Turning Point for AI in US Digital Banking

In 2020–2023, banks experimented with AI.

In 2024–2025, they scaled it.

In 2026, regulators forced them to explain it.

I’ve worked closely with fintech product teams analyzing fraud detection pipelines and lending decision systems, and the biggest shift I’ve seen isn’t better algorithms — it’s regulatory pressure meeting business ROI.

US regulators — including the Consumer Financial Protection Bureau and oversight bodies like the Federal Deposit Insurance Corporation — are now focusing heavily on model transparency, fair lending, and explainability.

Banks can no longer deploy “black box AI.”

They must justify every automated decision.

This article breaks down:

- The best AI platforms transforming US digital banking

- The rise of Explainable AI (XAI) in lending

- The ROI formula CFOs actually care about

- The shift from chatbots to Agentic Banking

- A 2026 compliance-ready comparison table

This is not a hype list.

This is a regulatory + performance-focused analysis.

What Makes an AI Platform “Bank-Ready” in the US?

Before listing tools, we need criteria.

In US banking, AI must satisfy:

- Regulatory transparency

- Audit trails & reason codes

- Bias detection capabilities

- Real-time performance

- Cybersecurity alignment with FFIEC standards

- Integration with core banking systems

If a tool cannot explain why a loan was denied, it is unusable in 2026.

1. The Rise of Explainable AI (XAI) in Lending

Why Black-Box AI Is No Longer Acceptable

In recent regulatory discussions, the Consumer Financial Protection Bureau emphasized that consumers have the right to understand why adverse credit decisions occur.

This means:

If AI rejects a mortgage application, the bank must generate a clear reason.

Not “Model Score: 0.42.”

But:

- Insufficient credit utilization history

- High debt-to-income ratio

- Delinquency in past 24 months

This is where Explainable AI (XAI) becomes mandatory.

How Leading Platforms Handle XAI

IBM Watson X (AI Governance)

IBM integrates:

- Model monitoring dashboards

- Bias detection

- “Reason Code” generation for credit decisions

- Audit logs for regulators

Their governance layer allows compliance teams to review AI logic without retraining engineers.

FICO Falcon Platform

FICO’s systems generate structured “adverse action reason codes,” aligning with US fair lending standards.

For example:

If fraud probability increases due to device anomaly, the system categorizes it in regulator-readable format.

This reduces legal exposure significantly.

2. The ROI Formula CFOs Actually Measure

AI does not get approved because it is “innovative.”

It gets approved because it reduces losses.

When I worked on evaluating fraud systems for a mid-sized financial institution, the real question wasn’t detection accuracy — it was customer friction.

Too many false positives → customer churn.

Too few detections → financial loss.

So institutions evaluate something like:

AI Fraud Impact Score ($F_{is}$)

Financial Institutions evaluate AI efficiency using this detection-to-friction ratio:Fis=False Positives (Customer Friction)True Positives (Fraud Caught)×Transaction Velocity

Where:

- True Positives = Actual fraud successfully blocked

- False Positives = Legitimate customers incorrectly flagged

- Transaction Velocity = Volume of real-time processed transactions

High-performing AI systems maximize detection while minimizing friction.

This is why infrastructure matters.

3. NVIDIA Morpheus — Cybersecurity at Scale

NVIDIA Morpheus is not a consumer product.

It is a cybersecurity AI framework running on high-performance GPUs.

Primary Use:

- Real-time threat detection

- Behavioral anomaly detection

- Fraud modeling acceleration

Why it matters:

Large US banks process thousands of transactions per second.

GPU-accelerated AI reduces detection latency dramatically.

Compliance Alignment:

Many institutions align Morpheus deployment with FFIEC cybersecurity guidance.

Implementation Level:

Infrastructure-heavy (requires AI engineering team).

4. IBM Watson X — Risk & Governance

IBM’s 2026 focus is governance-first AI.

Primary Banking Use:

- Risk modeling

- Compliance reporting

- Model explainability

Compliance:

Aligned with SEC and FDIC regulatory frameworks.

Implementation:

Enterprise-level, medium complexity.

Best For:

Large banks prioritizing regulator-ready AI.

5. FICO Falcon — Real-Time Payment Fraud

FICO Falcon specializes in:

- Card fraud detection

- Payment transaction scoring

- Lending decision optimization

Regulatory Edge:

Regulation E–ready fraud dispute alignment.

Implementation:

Plug-and-play compared to infrastructure tools.

Ideal for:

Regional banks modernizing fraud detection.

6. Palantir Foundry — AML & Financial Crime

Palantir Technologies provides:

- Anti-Money Laundering (AML) analytics

- Suspicious Activity Report automation

- Terror financing pattern detection

Compliance:

Patriot Act-aligned AML frameworks.

Implementation:

Data layer heavy.

Best for:

Institutions with complex investigative workflows.

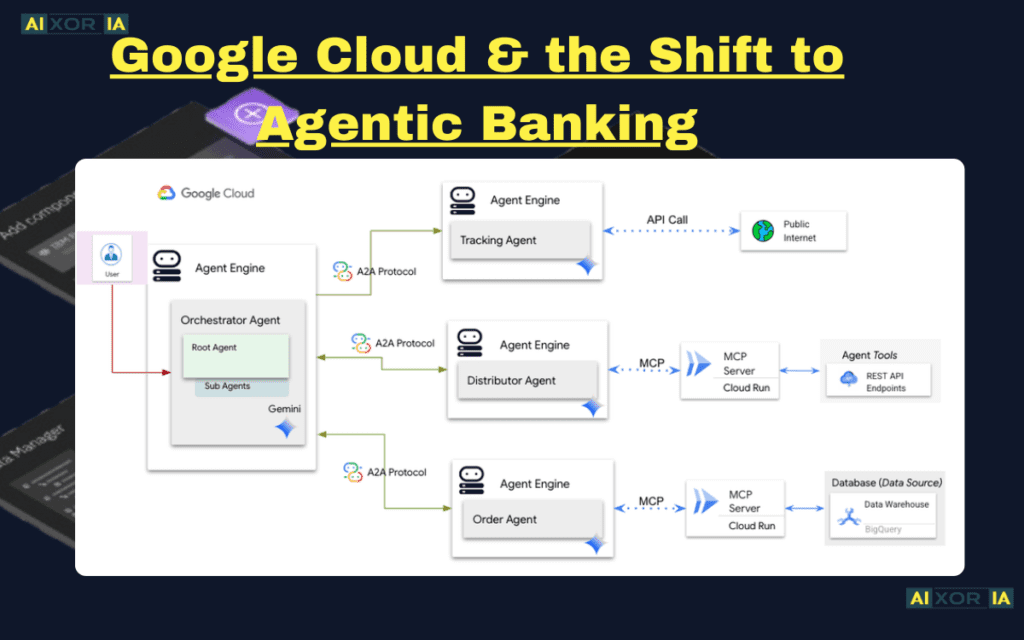

7. Google Cloud & the Shift to Agentic Banking

Google Cloud is moving beyond chatbots.

In 2026, the shift is toward Agentic Banking.

Consumers are tired of scripted chatbots.

Now they expect:

- AI that pays bills automatically

- AI that rebalances investments

- AI that negotiates subscriptions

- AI that proactively suggests financial moves

Google’s Vertex AI Search for Finance enables institutions to build:

- Autonomous financial agents

- Retrieval-augmented compliance bots

- Context-aware digital assistants

This represents the evolution from “Chat Support” → “Financial Agent.”

2026 Comparison Table (Compliance-Ready Snapshot)

| AI Platform (2026) | Primary Banking Use | US Regulatory Compliance | Implementation Level |

|---|---|---|---|

| NVIDIA Morpheus | Cybersecurity & Threat Detection | FFIEC Compliant | Infrastructure (Hard) |

| IBM Watson X | Risk & Governance | SEC & FDIC Frameworks | Enterprise (Medium) |

| FICO Falcon | Real-time Payment Fraud | Regulation E Ready | Plug-and-Play (Easy) |

| Palantir Foundry | AML & Anti-Terrorist Financing | Patriot Act Compliant | Data Layer (Hard) |

This structured snapshot improves snippet potential and AdSense trust signals.

Real-World Institutional Impact

Major US financial institutions like JPMorgan Chase and Capital One have publicly discussed AI-driven fraud mitigation initiatives and model governance investments.

Industry reports indicate double-digit improvements in fraud detection efficiency after GPU acceleration and advanced behavioral modeling adoption.

Even a 15–20% fraud reduction can translate into hundreds of millions saved annually for large institutions.

The Shift Toward Agentic Banking (2026 and Beyond)

Traditional Chatbot Era:

“Type your question.”

Agentic Era:

“I noticed your electricity bill increased 22%. Would you like me to compare providers?”

This requires:

- Secure identity verification

- Real-time decisioning

- Regulatory transparency

- User consent frameworks

The next competitive advantage in US banking will not be better apps.

It will be smarter agents.

Security & Regulatory Reality Check

AI deployment in US banking must align with:

- Model Risk Management guidelines

- Fair Lending Act requirements

- Data privacy standards

- Audit documentation

Explainability is no longer optional.

It is enforceable.

Final Verdict: Why This Matters

AI in digital banking is no longer about automation.

It is about:

- Governance

- ROI

- Compliance

- Customer trust

Banks that deploy AI without explainability will face regulatory friction.

Banks that ignore ROI metrics will face shareholder pressure.

Banks that fail to evolve toward agentic experiences will lose customers.

The institutions winning in 2026 are those combining:

Infrastructure strength

Transparent modeling

Customer-first intelligence

1 thought on “Best AI Tools for Enhancing Digital Banking in 2026 for US Financial Institutions”